The Travel Market Report from BCD Travel’s Research & Intelligence team offers insights into current trends in the travel industry.

- The report starts with a global airline industry outlook from the International Air Transport Association (IATA), covering six regions.

- It compares American Airlines’ updated Q2 2024 outlook with the financial performance of Delta Air Lines and United Airlines over the past year.

- It explores the increase in bilateral partnerships among airlines, including new and expanded codeshare agreements.

- Global trends in hotel room rates are analyzed using an index of average daily rates.

- The report also presents key findings from surveys of travel managers/buyers and business travelers on travel policy, with detailed reports to follow.

Welcome to the latest edition of the Travel Market Report, brought to you by BCD Travel’s Research & Intelligence team.

We start this quarter’s Travel Market Report with a roundup of the latest global airline industry outlook from the International Air Transport Association (IATA). This includes a summary of what to expect in six regions.

American Airlines has recently adjusted its outlook for the second quarter of 2024. We explore how its financial performance over the last 12 months has compared to its rivals Delta Air Lines and United Airlines.

Sticking with airlines, more appear to be striking bilateral partnerships, including new or expanded codeshare arrangements. Guided by recent examples, we try to understand what factors may be driving this.

Turning to hotels, we use an index of average daily rates to understand how room rates are trending around the world.

Finally, as part of our program of regularly surveying both travel managers/buyers and business travelers, we’ve taken the opportunity to get both groups’ views on travel policy. You can learn about some of the key findings, before delving into the detailed reports, once they are both published.

The Research & Intelligence team

Mike Eggleton

Director, Research & Intelligence

Natalia Tretyakevich

Senior Manager, Research & Intelligence

Melina Sibaja

Travel Insights Analyst

Global airline industry outlook

Outlook for 2024 improves

The International Air Transport Association (IATA) expects airline industry revenue to reach $996 billion in 2024, up almost 10% year-over-year (YoY) and reaching the highest nominal value in its history. The primary driver of growth will be an increase in traffic, with global airline passenger revenues forecasted to increase by more than 15% to $744 billion.

Global air travel should finally fully recover in 2024, with passengers expected to number almost 5 billion. While up 10.4% YoY from 4.45 billion, the figure will also be 9% higher than in 2019. Traffic (revenue passenger kilometers – RPKs) should grow at a slightly higher pace of 11.6%, as people increasingly take longer trips. This will help support a 4.3% rise in average ticket prices (ATPs) globally, although this will be much lower than 2023’s 15% increase.

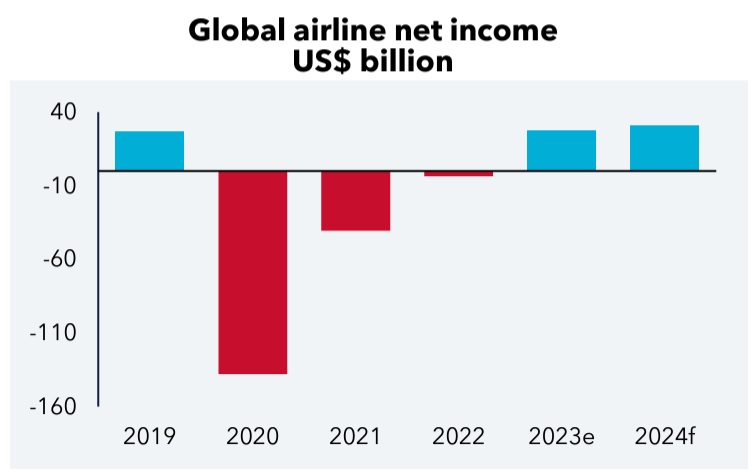

Since its previous forecast (December 2023), IATA has raised by almost one-fifth both its global airline net profit estimate for2023 and its forecast for 2024. It’s also increased from 10.3% to 11.3% the pace at which it expects profits to grow in 2024.

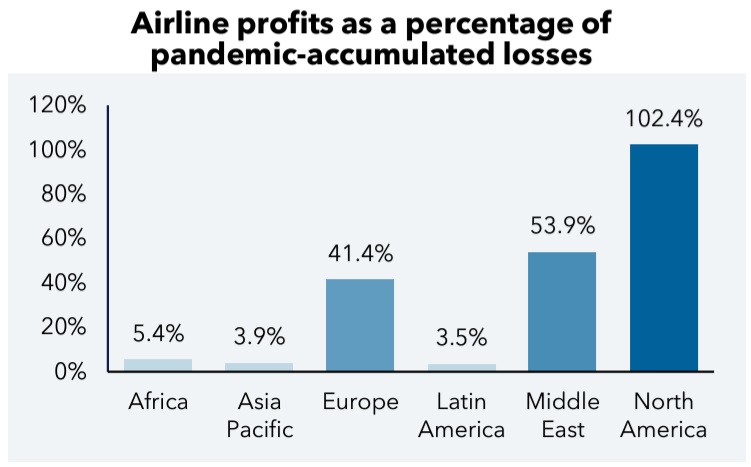

Between 2020 and 2022, the world’s airlines had accumulated almost $182 billion in net losses; they’re scheduled to deliver total profits of $58 billion for the 2023-2024 period. It’s clear they still have a long way to go to fully offset the damage done by the pandemic to their bottom lines. But airlines in some regions are making better progress than others elsewhere.

In 2024, airlines in Africa, Asia Pacific and Latin America may only have generated sufficient profits to offset 3 – 5% of total losses built up during the pandemic. European and Middle Eastern carriers are likely to have made much more progress, eating into 40 – 50% of their pandemic losses. But it’s North American airlines that are leading the financial recovery. This year, IATA expects them to have built up enough profits to more than cover total pandemic losses, putting them in a solid position going forward.

Regional prospects for 2024

Africa – while demand for air travel exists, it’s being held back by high costs, while geopolitical issues will weigh on airline profits.

Europe – travel demand will remain strong, but supply chain issues and the risk of labor disputes remain challenges to European airline finances.

Middle East – significant traffic growth supported a strong financial performance among the region’s airlines in 2023. Gulf hub operations located in an economically buoyant region offer encouraging prospects for airlines in 2024.

Asia Pacific – 2023’s slower than hoped for rebound means airlines may enjoy a bigger boost to growth in 2024 from the delayed release of pent-up demand for international travel.

Latin America – some airlines face considerable financial difficulty, reflecting the region’s economic and social turmoil. Markets in Central America will be key to driving growth.

North America – solid consumer spending and robust air travel demand are expected to continue underpinning airline finances. Labor shortages may impact smaller regional markets.

U.S. airline performance

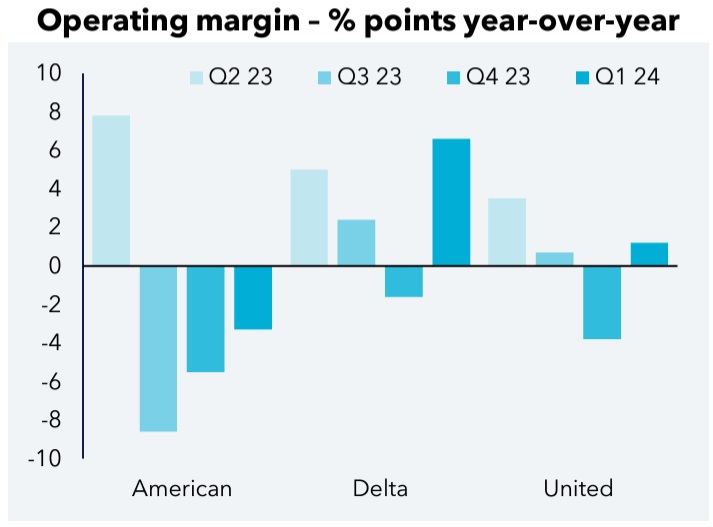

American Airlines’ performance lags its rivals

Weaker-than-expected bookings prompted American Airlines to lower its operating margin expectations for the second quarter of 2024 by one percentage point to an 8.5 – 10.5% range. This is a big reduction on last year’s second quarter, when the airline posted a 15.4%margin. In part, American’s CEO, Robert Isom, blamed the downgrade on some of the changes the airline had made over the last year to its sales and distribution strategy. He also cited a weaker-than-expected domestic pricing environment caused by a supply and demand imbalance.

Given this announcement, it’s worth comparing American Airlines’ financial performance over the last four reported quarters to that of its rivals Delta Air Lines and United Airlines.

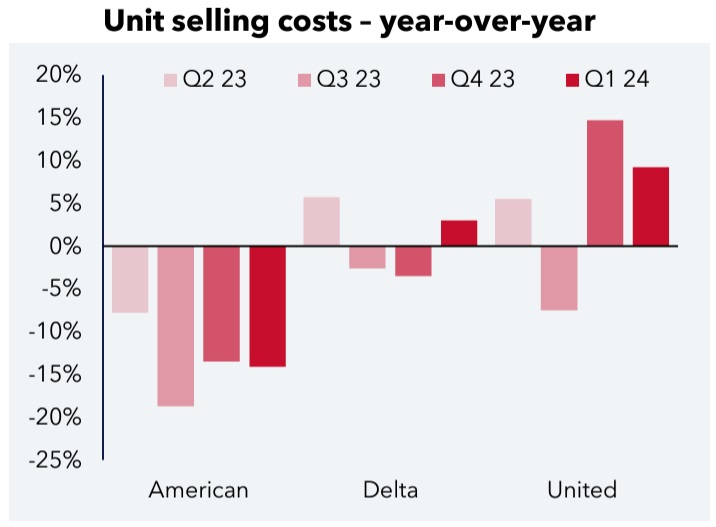

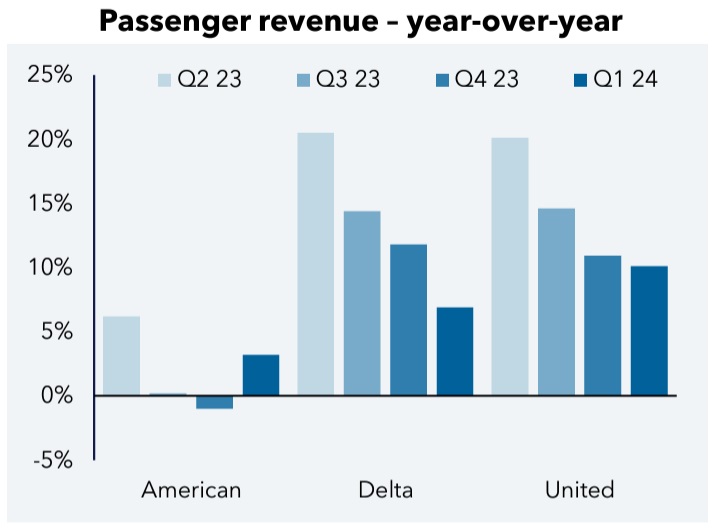

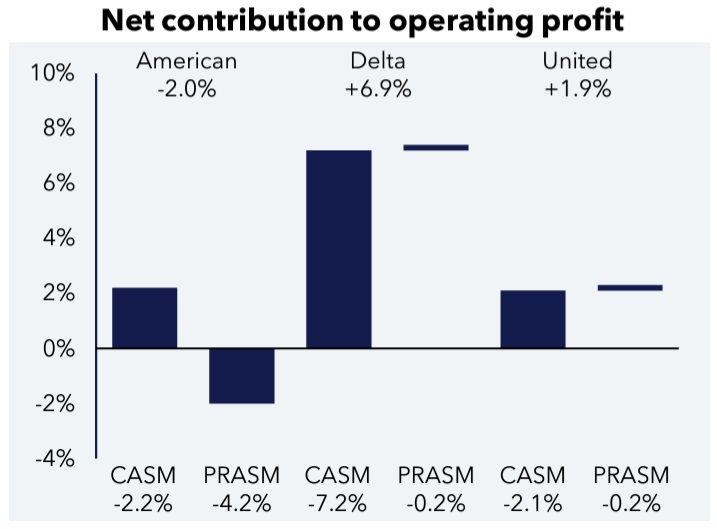

The benefits of American’s changed distribution strategy are clear. It has reported lower unit selling costs year-over-year (YoY) in each of the last four quarters; something its rivals have failed to match. But this has coincided with a poor revenue performance compared to its competitors. Passenger revenue at American in the Q2 2023-Q1 2024 period increased by just 2.1% YoY. Both Delta and United lifted their revenues by close to 14%. Worse still, while unit revenues (PRASM)1 at both airlines were essentially flat, American’s fell by 4.2%.

While American has done a better job than its competitors in reducing its selling costs, it’s been much less effective in controlling total costs. Over the same four-quarter period, it reduced total unit costs (CASM)2 by 2.2%, a figure matched by United Airlines but bettered by Delta, which reduced its CASM by 7.2%.

In essence, American has seen unit revenue fall more quickly than unit cost, and this has weighed on its operating margins, which have been lower YoY in each of the last three quarters. Quite simply, a lower CASM contributes positively to profits, but a lower PRASM has a negative impact of profitability. In the Q2 2023 – Q1 2024 period, this imbalance between revenue and cost movements resulted in a negative net contribution to operating profits. At the same time, Delta and United struck a more productive balance between revenue and cost, making positive contributions to profitability of 6.9% and 1.9%, respectively. It’s no surprise that American has had to scale back its profit ambitions.

Source: BCD analysis of airline financial reports; (1) Passenger revenue per available seat mile (PRASM); Cost per ASM (CASM)

Airline alliances – bilateral codeshares ramp up

Airlines are increasingly forming bilateral partnerships

While consolidation through acquisition and merger continues with varying degrees of success around the world, alliance activity between individual airlines has stepped up in recent months. There are some changes in store for global alliance membership. SAS is due to switch from the Star Alliance to SkyTeam in September. Italian carrier ITA Airways seems destined for the Star Alliance, and Fiji Airways will upgrade to full membership of Oneworld over the next 12 months. But most activity has been at the bilateral level, with individual airlines agreeing new codeshare partnerships. Aside from customers benefiting from a seamless travel experience (under a single airline code), there are multiple strategic reasons for airlines pursuing these arrangements.

Strengthening global alliance linkages

The three global airline alliances and their memberships are now fairly well-established, with many member airlines code sharing with one another. But even today, there are still gaps; some airlines have yet to work bilaterally with all other members. It doesn’t always make sense. That said, progress towards fully-connected alliances, where all members are commercially linked with one another, continues. This is demonstrated by new codeshares announced between Star Alliance members Air China and Turkish Airlines, and between SkyTeam members Saudia and Virgin Atlantic. And more activity may be expected from SAS as its SkyTeam membership approaches.

Lining up new global alliance members

As alliance membership nears, you’ll often see new joiners doing deals with existing members. Talks between Virgin Atlantic and SAS are a prime example. But when impending membership has not been announced, bilateral activity can sometimes hint at an airline’s future destination. Take Indian carrier IndiGo. As part of its aspirations to build a global presence, it’s been implementing codeshares with multiple airlines. It already has deals in place with three SkyTeam carriers– Air France, KLM and Virgin Atlantic – as well as with Star’s Turkish Airlines. But could Oneworld membership be on the cards for IndiGo? Its latest codeshare is with Japan Airlines, which joins American Airlines, British Airways, Malaysia Airlines, Qantas and Qatar Airways among the Oneworld members to have deals with the Indian airline. At this stage, this is pure speculation, but such bilateral arrangements can be a good test of an airline’s credentials and commercial value before it’s invited into a multilateral arrangement.

Extending network reach

Marketing on another carrier’s flights can extend an airline’s network reach to destinations where it doesn’t make sense to operate its own services. It may lack the resources; there might not be enough demand; it may not have the traffic rights. A typical example is Air Baltic’s codeshare with Bulgaria Air, which means the Latvian carrier can now offer connections from Riga to Varna via Sofia, adding a new Bulgarian destination to its network without the need to fly there itself. Riyadh Air presents a more extreme case. Having earlier signed a cooperation agreement with Turkish Airlines, the Saudi carrier has recently agreed deals with Air China and Singapore Airlines, a year before it has even operated its first flight. But when it does launch, these deals mean Riyadh Air can immediately offer customers access to a much more extensive network. Through these three links exclusively with Star Alliance members, it’s possible that Riyadh Air may also be paving the way to be the group’s representative in the Saudi market.

Increasing presence

Sometimes it’s hard to fathom out exactly why two airline have partnered. Take the recent deal between Emirates and Icelandair. Demand between Iceland and the U.A.E. doesn’t seem to justify the relationship; it doesn’t even justify direct scheduled air services between the two countries. By adding its code to Icelandair’s flights, Emirates will gain visibility in the Icelandic market, increasing its marketing power when travelers are reviewing their choices to the Middle East and beyond.

Hotel performance – a regional view of pricing

Amore stable trend in hotel pricing has emerged

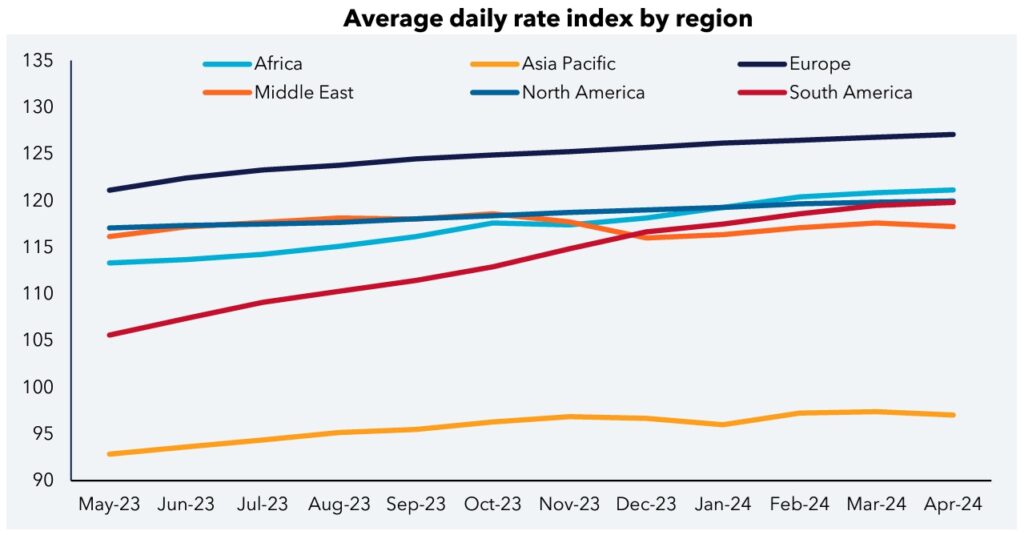

By creating an index based on a 12-month moving average (Dec. 2019=100), it’s possible use average daily rate (ADR) numbers from STR to identify underlying trends in hotel pricing around the world.

Rates have so far posted their strongest recovery in Europe, and they are continuing to trend higher, with the index rising by more than 6% over the last 12 months. But it’s South America’s hotels that have seen the biggest surge in pricing, with ADRs trending 15% higher.

In recent months, prices have stabilized in most regions, including South America. Even in the Middle East, the price index has become steadier after falling during the final quarter of 2023.

While Europe stands out for its stronger performance, Asia Pacific is more obviously the weakest performing region. Its ADR index is still 3% below its pre-pandemic level and has shown little sign of making further progress so far in 2024.

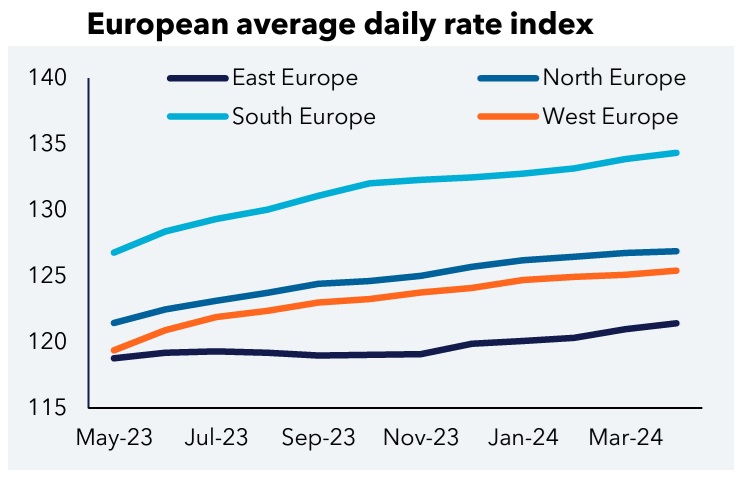

European hotel rate trend

Europe’s rate recovery has so far been strongest in markets in South Europe, and this sub-region continues to drive pricing, with the ADR index rising by 7.5% in the last 12 months. In contrast, hotels in East Europe have been the least successful in pushing rates up beyond their pre-pandemic levels and have secured only a 3.6% rise in the index. But there are signs of pricing picking up more quickly in recent months.

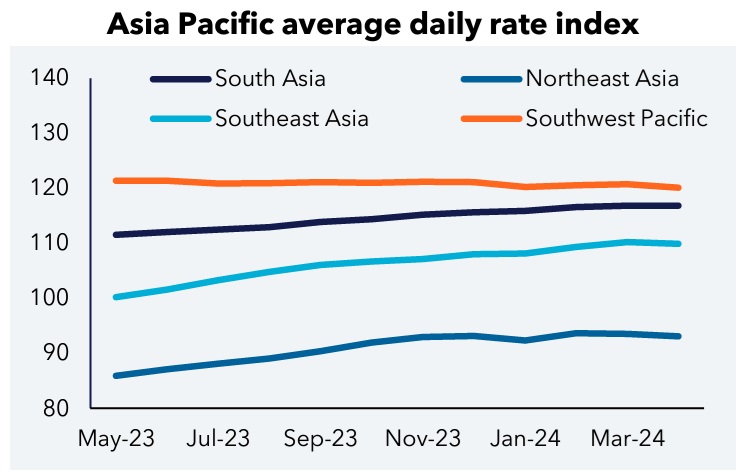

Asia Pacific hotel rate trend 140

Southwest Pacific led the recovery in rates in Asia Pacific, but they now appear to have hit a ceiling, with the ADR index settling at a level 20% higher than before the pandemic. Northeast Asia has been holding back the region’s rate recovery. Its ADR index has yet to move back above 100. And while it has risen by 11% over the last 12 months, it’s made little progress since the end of 2023.

Travel policy: travel buyer survey

Travel buyers told us about their company travel policies

In this survey we explored the state of modern corporate travel policies. We were particularly interested in looking at the policy changes happening in response to travel buyers’ shifting priorities, as well as exploring the new trends shaping business travel. The results are based on an online survey of 211 travel buyers conducted from April 3-17, 2024.

Our findings, at a glance

Travel program priorities

In descending order, travel buyers identified duty of care, cost control and policy compliance as their top three travel program priorities, with each increasing its rating since 2023. Ratings assigned to all other priorities have fallen slightly over the last 12 months.

Traveler satisfaction & wellbeing, which had ranked second last year, has slipped to fourth place, to be replaced in the top three by policy compliance. Similarly, payment & expense has fallen down the rankings to fifth spot.

Travel policy overview

Almost all (95%) travel buyers reported their company having a published travel policy, although more than threequarters had combined it with expense regulations into a single Travel and Expense policy. When describing the emphasis of their travel policy, almost 60% of buyers defined it as cost-focused, while a further 30% considered it to be traveler-centric.

Travel policy challenges

The biggest challenge when managing travel policies is traveler education: Almost two-thirds of travel buyers agreed. This is followed by working with policy exceptions, managing policy across different regions and countries, and controlling policy compliance, according to more than four in 10 buyers.

Mandated policies and prohibited suppliers

Among the various travel policy elements, air class is mandated most frequently: Nine in 10 travel buyers indicated this. Over half mandate the use of corporate cards, car rental class and meal allowance.

Rail suppliers are mandated the least, and this also means few regulations around use of rail instead of air. Rather than modes of travel, policies tend to prohibit specific travel suppliers: Sharing economy accommodation is banned by four out of five policies. Around three in 10 do not allow the use of serviced apartments and chauffeured cars

Travel policy trends

Almost two-thirds of travel buyers expect sustainability, along with safety and security, to exert the strongest impact on corporate travel policies in the years ahead. While duty of care has been the top travel program priority for some time, sustainability currently props up the bottom of the list.

Technology is also rated as an important trend by more than half of travel buyers. A further 46% see IATA’s NDC as something to watch. Meanwhile, DE&I finds itself at the bottom of the list of trend alongside bleisure travel: Both are recognized as trends but are not regarded to have a material impact on travel policies.

Find out more

We’ve highlighted just some of the travel policy survey’s key findings. You can find out much more in the full report using this link .

Travel policy: traveler survey

Business travelers gave their perspective on corporate travel policies

In this second survey, we explored corporate travel policies from the business traveler’s perspective. This included an exploration of the changes happening to policies and an assessment of traveler satisfaction with current regulations.

The results are based on an online survey of 1,201 business travelers worldwide. The survey was conducted from April 10-19, 2024.

Our findings, at a glance

Travel policy overview

Almost all (96%) travelers reported having a published travel policy in their company. Encouragingly, an equally high proportion of traveling employees know where to find the policy, when it’s needed. Such policies are typically cost-focused, according to half of respondents.

When planning a business trip, nine out of 10 travelers consult the travel policy, with a quarter doing so frequently. Eight out of 10 have checked their company’s travel policy in the past 12 months.

Travel policy and employment

A company’s travel policy does not appear to be an enticement for new joiners, with just 8% citing it as a factor when accepting a new job. In fact, over half did not receive any details about their prospective employer’s travel policy during interview. But travel policy has a role to play in retention, with a quarter of employees acknowledging its influence over their willingness to stay with a company.

Out-of-policy deviations

While one-third of business travelers never deviate from the company’s travel policy, most behave out of policy from time to time. Client meetings may require booking out-of-policy transportation or accommodation, just as travelers visiting conferences and events may need to use non-preferred or more expensive travel suppliers.

As a consequence of non-compliant behavior, traveling employees often need additional approvals. Also, reimbursement of out-of-policy travel expenses may be challenging.

Traveler satisfaction

Business travelers have mixed reviews about policy. Half of travelers are satisfied with their travel policy, but more than one-fifth said their policy isn’t responsive to traveler needs or is too restrictive. And yet one-third reported no issues with their company’s travel policy.

Air and hotel ancillaries

Company travel policies most often include such air ancillaries as seat selection, onboard food and beverages and extra baggage. Class upgrades and lounge access are rarely available but are the most demanded: Three quarters of travelers were interested in these services, as well as priority boarding.

When it comes to accommodation, six in 10 travelers have Wi-Fi and room service available, but the room minibar and entertainment are rarely covered, although few travelers were interested in these options. But two-thirds would like their travel policy to allow room upgrades .Almost half were also interested in early check-in and late check-outs.

Find out more

We’ve highlighted just some of the travel policy survey’s key findings. You can find out much more in the full report that will be published soon.