In the Q3 2023 report we highlight trends shaping travel’s future, explore the prospects for inflation, take a close look at airfares in Asia, catch up on hotel rates around the world, summarize what travel buyers told us about payment and expense, and finish with key findings from travelers and travel buyers about sustainability.

Welcome to the third edition of the Travel Market Report, brought to you by BCD Travel’s Research & Intelligence team.

In this quarter’s Travel Market Report, we address the following issues:

- Inspired by a report from Skift, we start by sharing our take on six trends which we expect to shape travel’s future.

- Most of us have been impacted by the cost of living crisis, as inflation has soared in many countries. But what are the prospects for inflation? We take a closer look at the outlook and the emerging problem of sticky inflation.

- In previous editions of the Travel Market Report, we’ve looked at European and U.S. airfares; now it’s the turn of fares in Asia Pacific to go under the microscope, as we take a closer look at China, India and Japan.

- In what’s become a regular feature in the Travel Market Report, we catch up on the latest on hotel rates around the world. We take a closer look at what’s happening in Asia Pacific, Europe, North America and South America, which are at different stages in their recoveries.

- In the previous quarter’s Travel Market Report, we shared our survey insights on what travelers thought of payment and expense. Now it’s the turn of travel buyers, as we explore the key findings of our second global survey this year on this subject.

- And last but certainly not least, we close this quarter’s report with some thoughts on sustainability. We’ve recently surveyed both travel buyers and business travelers and we share their views on various aspects of sustainable travel.

The Research & Intelligence team

Mike Eggleton

Director, Research & Intelligence

Natalia Tretyakevich

Senior Manager, Research & Intelligence

Melina Sibaja

Travel Insights Analyst

Trends shaping travel’s future

An update of trends shaping the future of travel

Inspired by a recent report from Skift, we’ve outlined some of the underlying trends which could shape the future of travel over the medium-to-long term.

New ways of working: new ways of travel

While there has been a steady return to the office as the pandemic’s effects fade, hybrid-working, combining a mix of the office and various remote locations, looks set to stay. And of course, many employees have also made their transition to homeworking permanent.

Regular meetings with colleagues can provide the face-to-face contact remote workers lack. But this may require employees who rarely travel to do so more often. They may need extra support from travel managers.

Conferences, meetings and events will increasingly be used to bring teams together. Much can be learned from how established remote teams operate in this respect.

A polarized world

Most governments can impact (to varying degrees) where their citizens travel. They can even do this indirectly through domestic and international policies that influence the welcome their citizens might receive as visitors to certain countries.

If two countries are hostile towards one another, which seems to be increasingly the case these days, the consequences should be simple: They will limit travel between the two nations.

But it is often more nuanced than this as the world becomes more polarized, with differences between countries less obvious, the restrictions less tangible and harder to navigate.

Heightened uncertainty

The world has become geopolitically more complex. Changes to the established order have undoubtedly made the world less stable and increased uncertainty.

Russia’s invasion of Ukraine has forced a rethink of old alliances and efforts to create new ones. Friends have become enemies, enemies have become friends, and others try to stay on good terms with both.

The conflict in Ukraine highlights how quickly and widely uncertainty can spread. Ramifications have gone far beyond European security to include sharp hikes in global food and energy prices and instability in Africa, as proxy conflicts and disputes erupt, possibly with the aim of undermining western support for Ukraine.

Sustainable travel

The world is desperately trying to be greener, and so are large companies. And they’re facing growing pressure to act. Air travel is already firmly in the spotlight when companies set their environmental goals.

The louder consumers become about sustainability; the more companies are going to have to change the way they engage with the environment. This promises a much bigger effect on the business of travel.

An ageing planet

Economic powerhouse China is now experiencing a problem familiar to many advanced economies: an ageing workforce.

People are living longer and the increased burden they’re living under means they’re retiring later too. Travel will need to adjust to supporting the needs of an increasingly older workforce.

Technology accelerates

Artificial intelligence should come to the rescue of the ageing planet by boosting productivity of the diminishing workforce. It has many applications in travel, and many more we’ve not even imagined yet. It’s already being applied to respond to information requests, but more sophisticated applications will surely follow, touching most points of the business travel experience.

Source: Skift, July 31, 2023

What can we expect for inflation?

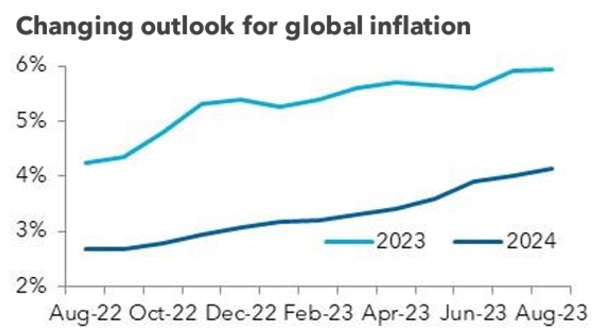

Inflation expectations continue to rise

Global inflation strengthened from 4.4% in 2021 to 8.2% in 2022, as supply chain issues, a surge in post-pandemic demand and soaring food and energy prices (largely associated with the war in Ukraine) fueled a sudden rise in the cost of living. As we’ve seen with airfares and hotel rates, travel did not escape this burst in inflation.

Inflation had been expected to slow rapidly in 2023: A year ago, Oxford Economics forecasted it would ease to 4.3%, but raised this figure to 5.4% six months later. And as we move through the current year, with central banks’ actions having had only limited success in reining in inflation, forecasts for 2023 have been steadily raised, with current expectations pushed up close to 6%. Expectations for inflation in 2024 have also been increased, from 2.7% in mid-2022 to 4.1% today. Inflation may no longer ease as rapidly as had been hoped.

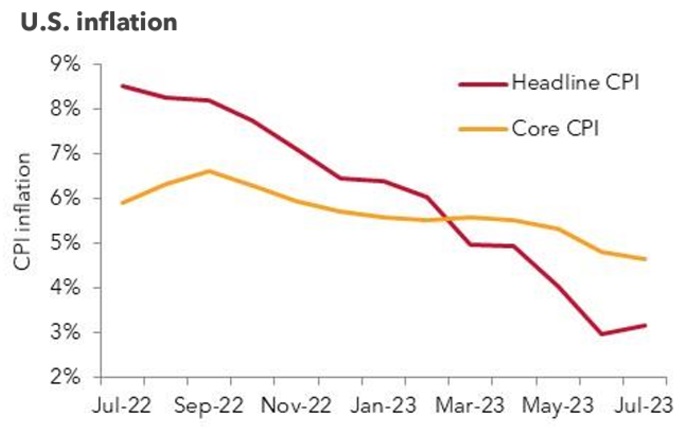

As headline inflation falls, as we cycle over the worst effects of 2022’s energy shock, core inflation (excluding food and energy) remains stubborn. In the U.S., while inflation has retreated from 8.5% to 3.2% over the last year, core inflation has only eased from 5.9% to 4.7%.

The consequences of central banks’ efforts to bring down this sticky inflation can be painful. Rising interest rates have pushed up housing costs and increased the risks faced by the most indebted countries. And yet inflation persists.

External forces may keep inflation elevated or even push it higher. Growing tensions between China and the U.S. over Taiwan have prompted companies to review their supply chains, often resulting in higher costs. Demands to increase public spending on emerging priorities, such as climate change and defense, will only add further pressure on inflation.

By raising interest rates, central banks could destroy enough demand to bring inflation down. But this risks inducing a recession. To avoid such a scenario playing out, central banks may instead choose to raise rates by less than is really needed and live with a higher rate of inflation, of say 3-4% (as opposed to the 2% they might be expected to target). The one problem with this approach is the financial markets, which have been pricing investments and debt on the assumption of 2% inflation over the next five years.

Higher inflation could force investors to switch into commodities, risking a price bubble, which itself could fuel inflation. Higher inflation would mean that the real value of debt falls. That’s good news for heavily indebted borrowers, including some governments. But lenders and bond investors could respond by simply increasing borrowing costs, affecting all borrowers. Faced with these risks, central banks will most likely adopt a course that lies between high inflation and recession, resulting in sticky inflation.

Source: BCD analysis

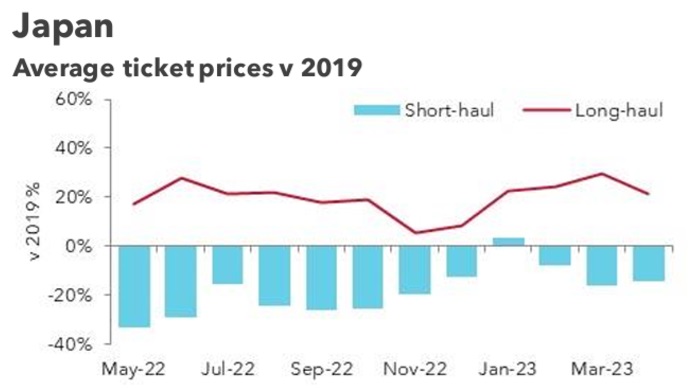

Airfares in key Asian markets

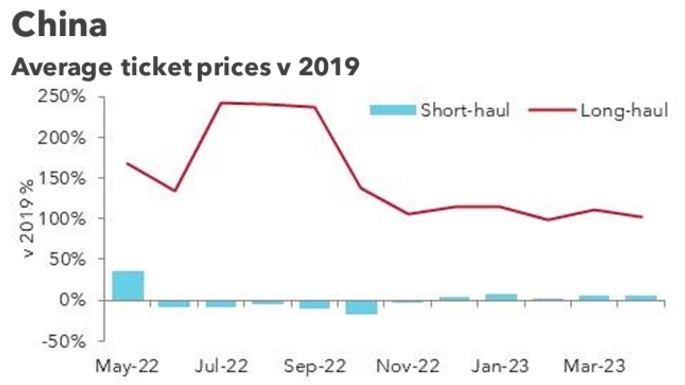

In mid-2022, long-haul fares surged 250% above 2019 levels. While rises have since moderated, fares are still twice their pre-pandemic level. Short-haul fares growth has been weaker, averaging 5% in March/April 2023.

Short-haul fares have yet to return to 2019 levels and were 17% lower in April 2023. But in the last 12 months, long-haul fares have been at least one-third higher, pushing on to 50% above 2019 in recent months.

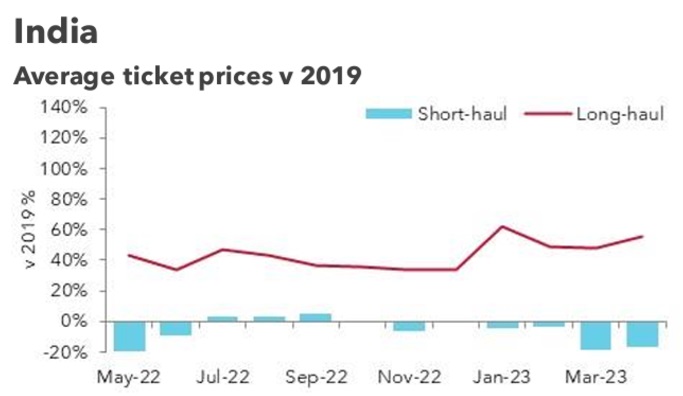

After moderating at the end of 2022, long-haul fares have returned close to 25% above 2019. While short-haul fares have made some progress, they’re still around 15% short of their pre-pandemic levels.

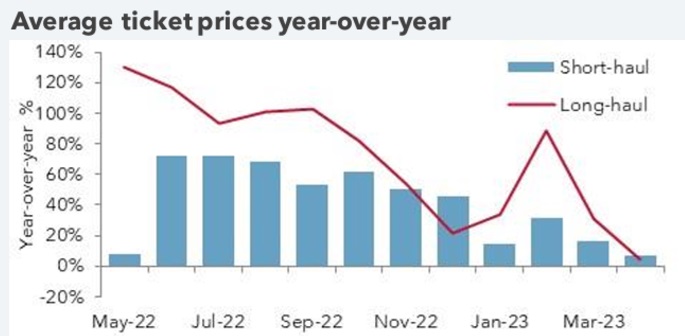

Year-over-year, a different picture emerges for long-haul fares. For much of 2023, they’ve been around one-fifth lower, as they cycle over 2022’s steep increases. Short-haul fares are erratic, rising by one-fifth in March but falling by a similar amount in April 2023.

Long-haul fares inflation has been on a downwards path. Cycling over some big increases last year, fares rose by just 4% in April 2023. Increases in short-haul fares are also trending lower, but more slowly. Increases in 2023 have ranged between 7% and 32%.

Short-haul fares have posted some strong year-over-year increases in 2023, strengthening from 17% in January to around 50% by March/April. After a period of weakness, long-haul fares rose by 6% in March, slowing to 2% in April.

Source: BCD Travel transactional data

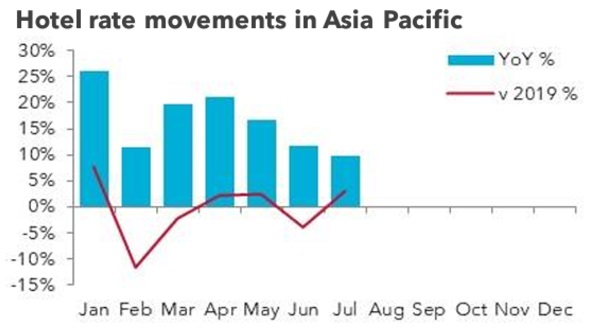

Hotel rates in Asia Pacific

Year-over-year rate movements are moderating

Having been as high as 25% at the start of the year, as 2023 has progressed, year-over-year movements in average daily rate (ADR) across Asia Pacific have Hotel rate movements in Asia Pacific moderated. By July, ADR inflation had eased to 10% and averaged 15% over the first seven months.

While these increases quickly pushed ADRs back to their 2019 levels, the recent easing has ensured they’ve not moved too much higher. Year-to-date, ADRs across Asia Pacific have been 1% lower than in 2019, although they were up by almost 5% in July.

Asia’s main markets are at different stages in their own recoveries. China’s situation is the one that most closely matches the regional position. From a peak in April, year-over-year ADR movements had fallen from 46% to 15% in July. Momentum created by the country’s reopening has not endured, but it could be reignited in the months ahead, as more travel restrictions are eased.

After a strong start to 2023, when ADRs increased by more than 50%, price rises +37% in India have moderated and stabilized. For the last three months, ADRs have risen on average by 14%, also remaining one-third higher than in 2019.

Japan, which reopened at the same time as China, has seen strong ADR rises sustained, exceeding 40% in May-July. There’s no immediate sign of rate inflation moderating any time soon.

Australia is in a completely different situation. In recent months, ADR inflation has been weak, and in July, rates dipped by 1%. But they remain 30% higher than pre-pandemic.

Source: Analysis of data from STR

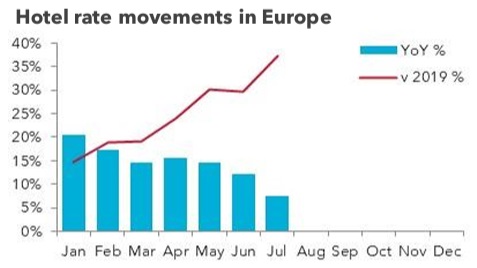

Hotel rates in Europe

Rates are moving higher v 2019

Year-over-year (YoY) movements in hotel average daily rates (ADRs) across Europe have eased from 21% in January to just 7% in July. Between June and July, rate inflation dipped by five-points; its most rapid easing so far this year.

While YoY rate inflation has moderated, and at a faster pace in recent months, the opposite has happened when comparing room prices to 2019.

From 15% at the start of 2023, average daily rates (ADRs) moved 37% above 2019 by July.

Many of Europe’s largest markets have largely mirrored the YoY trend. Both Spain and the U.K. have seen ADR increases ease as the year has progressed, each posting a 6% rise in July. And both markets have seen comparisons to 2019 prices remain around 30% higher.

Hotels in Germany and Italy appear to be on the same path, albeit a few months behind. Since April, rate increases have retreated from 24% to 12% in Italy and are holding steady at 50% above 2019. Germany has seen increases fall more rapidly, dropping from 30% in March to just 3% by July. It’s one of the few major European markets to see an easing of inflation compared to 2019.

Among this group of markets, France stands out. It had been following the other markets, with rate inflation easing as 2023 progressed. But, since June, ADRs have been rising more rapidly, increasing by 36% in July. Upwards movements have been even more pronounced when compared to 2019, surging by 87% most recently.

Source: Analysis of data from STR

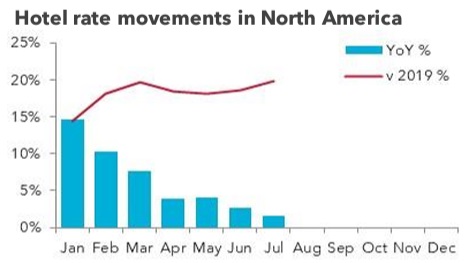

Hotel rates in North America

Year-over-year rate inflation is easing

After pausing in May, the rate at which average daily rates (ADRs) among North America’s hotels have been increasing year-over-year resumed its easing. By July, ADRs were up by just 2%.

Between March and July, however, ADRs have remained between 18% and 20% higher than they were in 2019. Despite the ever lower year-over-year movements, ADRs have pushed back recently to levels 20% above 2019.

Because of its sheer size, what happens in the U.S. effectively drives the regional picture. Since the start of 2023, ADR movements have retreated from 15% to just 1-2% in June and July. When compared to 2019, however, ADRs have stayed one-fifth higher throughout 2023.

While ADRs in Mexico have remained close to 30% above their pre-pandemic level, they’ve been falling year-over-year in every month since March. After an incremental shift down in June, ADRs fell by 13% in July.

Canada presents a mixed picture. While year-over-year price movements have eased this year, the rate of slowdown has been modest. By July, ADRs were still rising by 8%. And, having been close to one fifth above 2019 for much of 2023, this gap widened to 26% in July.

Source: Analysis of data from STR

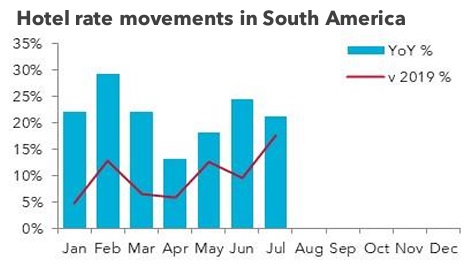

Hotel rates in South America

Rates inflation is strengthening again

Hotel rate inflation across South America had eased to 13% by April, but hotels have since regained some pricing power. By June, average daily rates (ADRs) had moved back almost one quarter higher year-over-year (YoY) and were more than one-fifth higher in July.

When compared to their pre-pandemic 2019 levels, ADRs this year in South America have also moved higher since April. From 5% above their 2019 level, room rates advanced to 18% higher by July.

Creating a regional view relies on aggregating ADRs denominated in US dollars. But if left in local currency (right), a more varied ADR performance across South America emerges.

In most cases, YoY movements have eased in recent months. It’s been more gradual in Colombia and Brazil, where ADRs increased in July by 18% and 11%, respectively. The slowdown in rate inflation has been more noticeable in Chile, where ADRs increased by just 1% in July, while Peru has gone even further, with ADRs 6% lower YoY.

The situation is different in Argentina, where ADRs are priced in dollars. Rate inflation remains high, with ADRs up by 29% in July, priced at 68% above their pre-pandemic level. Compared to 2019, ADRs have also remained 45-55% higher in Colombia and Brazil.

Source: Analysis of data from STR

Payment and expense: the travel buyer view

Travel buyers share their views

We continue our deep dive into payment and expense, this time exploring the topic from the point of view of travel buyers. What are travel buyers’ payment and expense priorities? What payment methods do travel programs offer today? What challenges do they encounter and how are these challenges addressed?

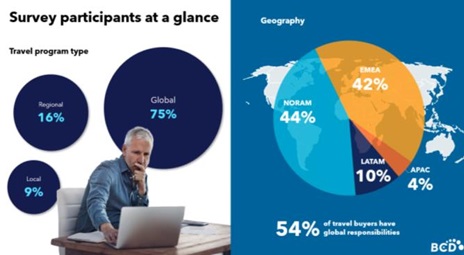

The answers to these questions and more are based on an online survey of 164 travel buyers we conducted in May 2023. We compared these insights with the results from the Payment & Expense survey we conducted in 2021 and the traveler views we collected in April 2023.

Most of our survey respondents are based either in North America (44%) or in Europe (42%). More than half (54%) have global responsibilities.

Survey findings at a glance

Payment and expense as a program priority

Out of all travel program priorities, payment and expense management has grown in importance the most, reaching its highest level in the last three years.

Since 2021, the percentage of travel buyers citing payment and expense management to be extremely or very important has grown from 76% to 88%.

Payment methods used in travel

Travel buyers report corporate cards as the most frequently used method, with 84% using them to pay for business travel.

Central billed accounts are also popular, mentioned by 7 in 10 travel buyers.

Virtual cards

Over a third of travel buyers offer virtual payments to their travelers. Nearly half are satisfied, while 3 in 10 say the opposite. A lack of awareness, as well as complicated setup and management are among the top reasons cited for not offering virtual cards.

Digital wallets

A third of travel buyers are interested in providing their travelers with a digital wallet that can store debit and credit cards, loyalty cards, tickets, etc. This falls short of traveler interest in digital wallets, which is much higher.

Integrated solutions

Nearly 6 in 10 travel buyers offer an integrated travel booking and expense solution that allows booking, managing and reporting on travel, all in one place. And of those yet to do so, a fifth plan to introduce them in the future.

Find out more

These are just a few of the survey’s key findings. You can find out much more in the full Surview report Travel Buyer Survey: Payment and Expense.

Source: BCD Travel survey, May 2023

Sustainability: traveler and travel buyer views

Travel buyer survey

During July 2023, we surveyed more than 100 travel buyers and almost 1,800 business travelers for their views on environmental sustainability and travel. With the help of travel buyers, we explored sustainability’s place in a travel program and examined travel management’s role in promoting sustainable travel. Surveying business travelers provided insights on their attitudes, motivations and behaviors towards sustainable travel.

The travel buyer view

Sustainability as a travel program priority

Two thirds of travel buyers rate environmentally sustainable travel as extremely or very important.

While 8 out of 10 confirm the availability of published sustainability goals within their companies, less than half have so far put in place targets for sustainable business travel.

Benefits and challenges

In addition to caring about the environment, travel buyers see enhanced company reputation and personnel recruitment as the top benefits from adopting a sustainable program. The biggest pain point on the way to adoption, however, arises from the elevated cost of sustainable travel options. Traveler education, a lack of standard measurement and providing the right tools are further issues to overcome.

Sustainability activities

At point of booking, two thirds of travel buyers provide flight emissions data. A further 44% use online booking tools (OBTs) showing emissions data provided by a selection of suppliers.

Less popular is carbon emissions offsetting’ It’s offered by less than a quarter of travel buyers, although 3 in 10 are considering it. And just one in six currently buys sustainable aviation fuel (SAF); something 22% have in their plans.

The business traveler view

Sustainable travel behavior

Taking fewer trips and sharing ground transportation when on a trip are the most commonly promoted sustainable travel choices. Almost half of travelers cite these as the top-two sustainable travel options encouraged by their employers.

The most popular sustainable practices embraced on the road relate to hotel stays. Some 7 in 10 travelers avoid changing their towels as frequently, and 6 in 10refrain from using daily housekeeping. Recycling and going paperless with travel documents are similarly as popular.

While over half of travelers are willing to take fewer but longer business trips, or try new, more sustainable ways of traveling, only 30% are prepared to pay more for such sustainable travel options.

Find out more

These are some of the two surveys’ key findings, but you can find out more in the full survey reports that will be published on www.bcdtravel.com September 2023.

Source: BCD Travel surveys, July,2023